Storage Wars - Decoding NSA's Unusual Options Volume of 8,000 Contracts

Originally shared on Jan 14th, 2026

If you follow me on Twitter, you might have noticed that I have been tweeting about CubeSmart and self storage REITs in general. Nick Huber, Sweaty Startup, had been very vocal about the attractiveness of self storage a few years back. I was always a bit shocked that people did not consider buying one of the large public self storage REITs instead. My understanding is that Bolt, Huber self storage company, has struggled with occupancy and cashflow. We have owned self storage in the past and generally view it as a great commercial real estate business model. Americans have a love affair with using self storage. We tend to own lots of stuff. Life events such as job loss, job gain, coming back from college, moving, divorce, etc all necessitate putting things in self storage. In the mid 2000s, people had doubts about the sustainability of self storage demand. Over time, self storage has proven to be a robust business model. After Q3 2025 earnings, most of the self storage REITs sold off across the board. We listened to the earnings call and couldn’t really find anything alarming. Again, it was mostly marginal stuff that is +/- 2% beat or miss against analysts’ expectations. If anything, it seems like there were finally green shoots in space after a prolonged period of elevated supply delivery, particularly in the Sunbelt. Rents, occupancy, and pricing power all seem to be trending in the right direction. High interest rates also hurt this business as there are less housing transactions and less people moving around the country. If interest rates are cut, it will have one additional benefit to self storage REITs on top of valuation and general benefits to the economy.

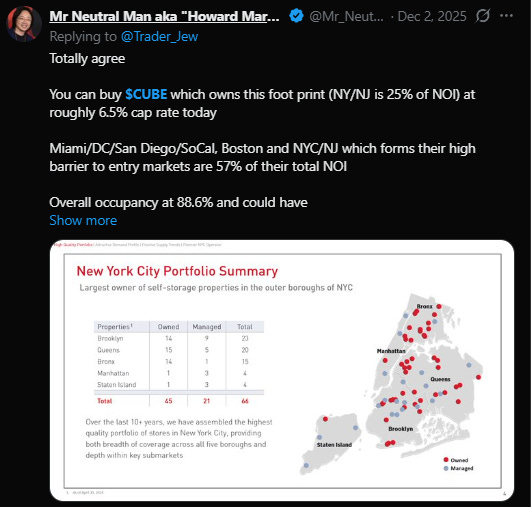

We aggressively bought CubeSmart at around $36 per share or roughly 6.8% cap rate. At $38 per share, the implied cap rate is roughly 6.5% and trades at roughly 14.6x P/FFO. It is currently one of our top five positions at over 10% of the portfolio. We thought this was an unbelievable valuation. We broadly believe that all of the self storage REITs are cheap to various degrees. But we particularly like CubeSmart. As real estate junkies, Calvin and I would marvel at CubeSmarts’ footprint in Brooklyn and Queens as we drove on the highway. NIMBYism is strong in a market like New York City and bringing on supply takes years. Politicians want housing, not self storage. We simply love this footprint. CubeSmart is able to charge one of the highest rent per square foot among all self storage REITs at roughly $23. Public Storage is a close second but trades at roughly a 100 bp lower cap rate than CubeSmart.

National Storage Affiliate (NSA)

About a week ago, I got a text from @air_real_estate who I met through twitter. I want to mention that I have gotten a tremendous amount of value out of Twitter. This is merely one example. If you see a “tea leave” like this and you would like me to take a look at a company or situation, please email me at hardasset2023@gmail.com or send me a Twitter DM @Mr_Neutral_Man

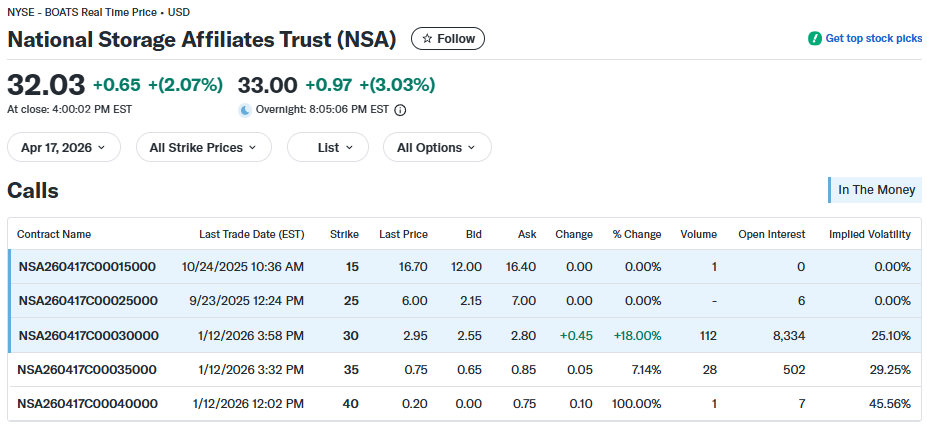

He mentioned that someone had bought over 8,000 options contracts of National Storage Affiliates Trust (NSA) April 17th, 2026 $30 strike options. The options activity was rather unusual. The nominal exposure (8,000 contracts X 100 contract per option X $30) is roughly $9 million dollars. I was immediately intrigued. Having met with National Storage Affiliates and reviewed their portfolio, our view is generally that it is cheap with an implied cap rate in the high 6% cap rate at the time. But NSA suffers from higher vacancy rates with occupancy at 84% at the end of Q3 2025. Its portfolio has heavier exposure to the Sunbelt which suffers from higher supply. Higher vacancy likely means having to offer concession and less ability to raise in place rent or Existing Customer Rate Increase (ECRI).

One of the changes that I made recently is to watch out for catalysts. If you have been a long time subscriber, you may notice that I have been weighting catalysts or events more frequently lately. This is because I have noticed that most REITs will trade cheaply until there is a reason to own the stock. In the case of NSA, this unusual options activity caught my eye. It is possible that someone might have insider information, i.e. NSA may be imminently acquired by a larger peer. However, options trading information is public information. Whether someone has material nonpublic information on NSA is pure speculation on our part. We are simply working with probability here. But $9 mm of notional exposure is A LOT of exposure to purchase in a single day. I thought about it and bought the same options within 24 hours for $1.65 per contract. This means that NSA stock has to rise to $31.65 by April 2026 for me to break even. Our position sizing is merely 0.2%, but it actually represents roughly 3% of notional exposure for the fund. The reason it is smaller is because NSA’s portfolio is lower quality.

In addition, @PerrySolem from Twitter has told me over the years that NSA’s management team is the least impressive of all the public REITs. Perry and I have grown to be good friends over the years with him occasionally crashing at my beach house when he is in New York City. Perry has provided invaluable insights into the self storage business. First, it costs as much as $170-180 per sqft to develop self storage in smaller markets. Second, Perry has noticed improvements in his own lease up of self storage units. If you are a large fund that is interested in investing in self storage REITs for 2026, I can make an introduction to Perry for consulting purposes. He knows the self storage development business inside and out. He can talk about replacement cost, financing cost, appetite of development equity capital (very little at the moment), real time rent and occupancy statistics. Perry has been instrumental in helping us develop our conviction in self storage REITs. The key takeaways is that CubeSmart and NSA are both trading at deep discounts to private market value.

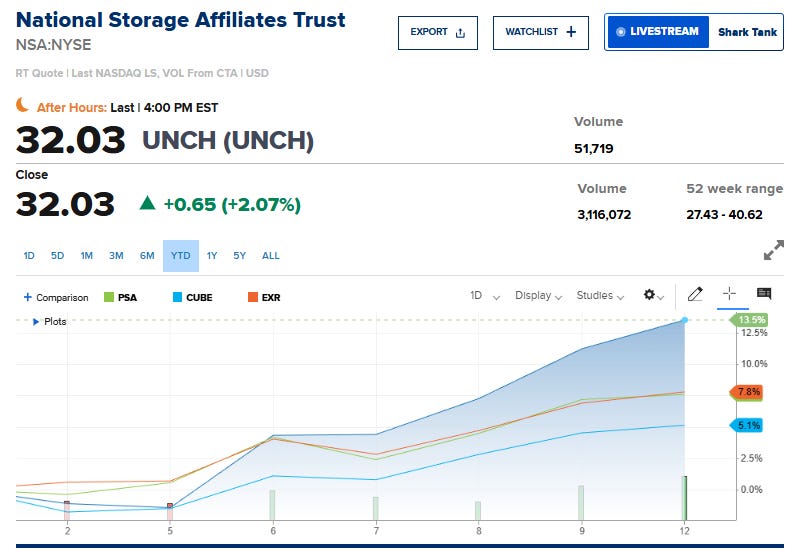

Year-to-date, NSA has outperformed all of its self storage peers by generating 13.5% return. Our NSA options, sized at 0.2% of the portfolio, have doubled. It would be interesting to see how NSA performs out in 2026. CubeSmart has experienced 5% gain year to date.

Valuation - Are the Self Storage REITs still cheap?

Is NSA Still cheap? I think so. We will hold onto our options and see what happens. A buyout will likely result in at least 20% premium to the current price. NSA’s occupancy is currently 84% and has lots more excess space to fill. It is both an opportunity and a curse. 16% vacancy likely means less ability to raise rent. But 16% vacancy also means more room to convert vacancy into high margin incremental NOI when fully leased. Portfolio occupancy had ranged from 87% to almost 93% in recent years. NSA’s same store occupancy ended Q3 2025 at 84.5%. NSA currently pays a 7.1% dividend and trades at roughly 6.6% cap rate and roughly 14.0 times P/FFO. NSA’s payout ratio is roughly 100%. If NOI or FFO were to drop, they may have to cut the dividend. It also carries more debt at 6.7x net debt/EBITDA. But NSA still covers interest expenses by a healthy 2.6 times. This is considered rather conservative by private real estate standards. But public REIT investors will generally view the balance sheet and interest coverage as “higher leverage.” In simple terms, NSA has more “torque” to the upside if self storage in the Sunbelt experiences occupancy and price gains.

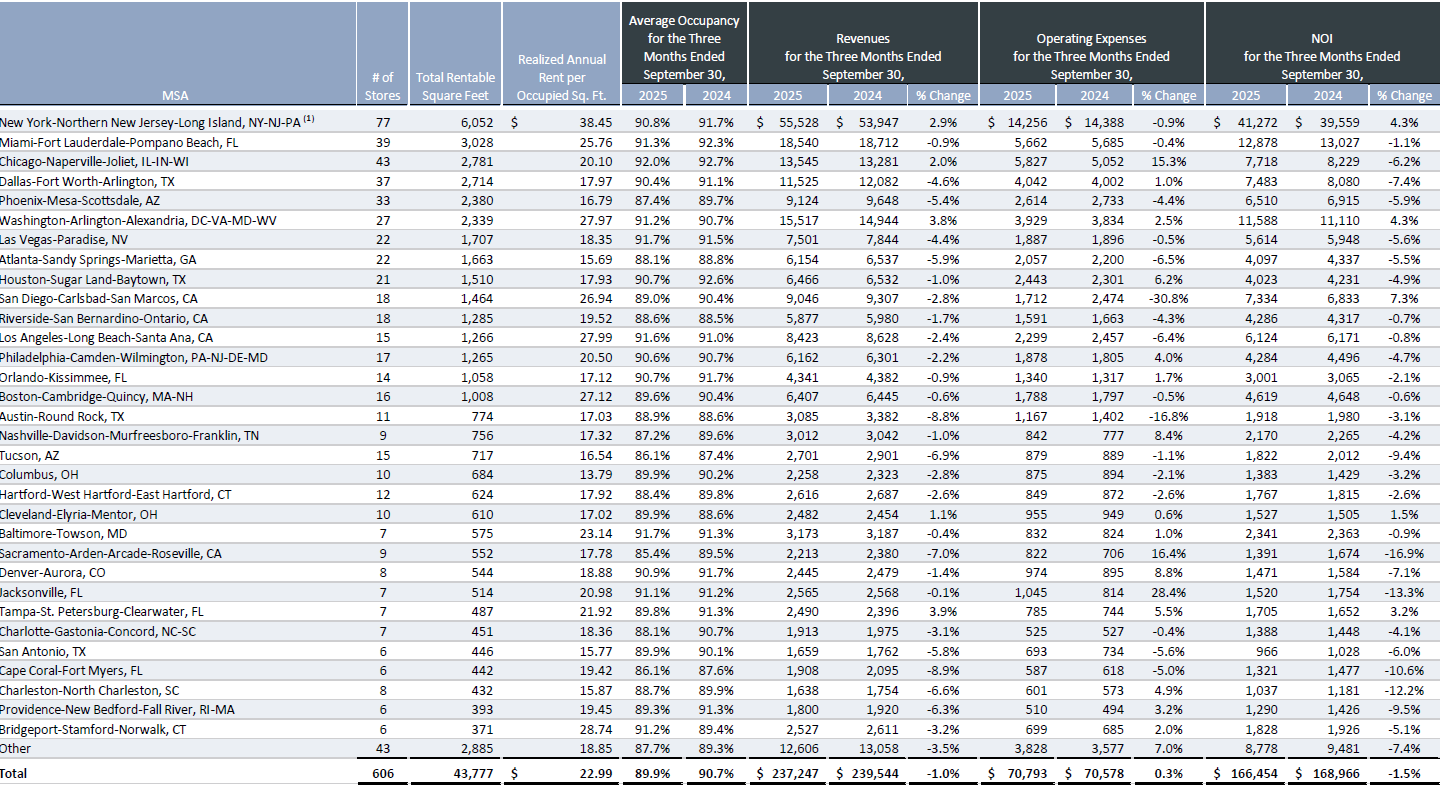

I do think CubeSmart is safer and owns a much better portfolio with half of their locations in lower supply and higher barrier markets like NYC, DC, SoCal, NorCal, Miami etc. Just look at this portfolio. CubeSmart is charging an average rent of $38.45 per sqft in NYC/NJ. This is probably 4 times what Nick Huber’s portfolio charges. NYC/NJ alone accounts for a quarter of CubeSmart’s overall NOI. Other markets that charge high rent are Miami at $26, DC at $28, San Diego at $27, and LA at $28. We believe that higher barrier markets account for 57% of the overall NOI. CubeSmart’s average portfolio rent of $22.99 is about 46% higher than NSA’s average rent of $15.70. Both REITs’ rents are significantly higher than Nick Huber’s Bolt portfolio. I would not be surprised if the average rent charged by Bolt’s portfolio is below $10 per sqft.

If you don’t have any self storage exposure, I think some combination of CubeSmart and NSA makes sense. I would probably put a higher weighting on CubeSmart. CubeSmart currently trades at roughly 6.5% cap rate and pays a 5.6% dividend at roughly 80% of FFO. CubeSmart covers its interest payments by an embarrassingly conservative ratio of 5.6 times. Since there are minimal maintenance cap ex, this is a very healthy payout ratio. Perry Solem told me that a $0.20 per sqft maintenance cap ex is reasonable for his properties. To be conservative, if we budget $0.50 per sqft in maintenance cap ex, CubeSmart can afford to payout up to 95% of the FFO since maintenance cap ex will be less than $25 million per year.

Unlike apartment REITs like Camden and MidAmerica where occupancy has stayed stable at 95%, we are likely buying at trough occupancy and trough rent. With some marginal increase in occupancy and rent/sqft, we believe that we could stabilize at over 7.0% cap rate for both REITs. CubeSmart could trade to 5.0% cap rate and NSA will likely trade to mid 5% cap rate. This sets up for a nice combo of price appreciation and dividend income. A 150 to 200 bps compression in cap rate is a huge driver of return while you collect nice dividends along the way. My friend Perry Solem can provide good information on private transaction comps and how buyers and sellers generally underwrite deals.

I think that investors can still generate over 20% IRRs by owning both REITs over a 3 year holding period through mostly price appreciation, NOI growth, and decent dividends. After the Fed increased interest rates in 2022, Cubesmart had traded as high as $54 in the fall of 2024 which would represent 42% upside plus dividends. NSA has traded as high as $48 which would represent 50% upside plus dividends.

Call To Action

If you manage self storage assets on the private side, I would love to exchange notes and thoughts with you. It would be especially valuable if you are willing to share real time rent and occupancy trends.