Alexander's ($ALX) Transformational Debt Restructuring at 731 Lex Ave

Originally written on Jan 2nd 2026

We wrote up our investment thesis for Alexander’s (Owns the Bloomberg Global HQ buildings in NYC) earlier in 2025 in the low $190s. Since then, the stock trades at about $218 and we are on target to receive $18 of dividends in 2025. At times, the stock traded as high as $260 in 2025. I have yet to update a detailed Net Asset Value adjusting for the dividends paid out and debt pay downs in 2025. But my current estimate is mid $300s or roughly 60% higher. The NNN Bloomberg lease has great escalators and potentially a big jump in rent in 2030. There is a scenario that NAV increases to over $400 per share in a few years. Best of all, we are receiving $18 or 8.2% in dividends per year. Alexander’s is in advanced negotiation on the sale of Rego I which is likely a $100 mm to $200 mm development site which would equate to roughly $19.6 to $39.21 per share of value. This could create a near term catalyst to pay out a large special dividend and it will likely increase NOI as it currently sits vacant incurring cost while generating minimum revenue. A lot has happened this year and they are almost all positive. Every development has proven that management is aligned with shareholders. There is also heavy short interest in the stock equal to 9-10% of the float. I believe that the short thesis is now broken as both large chunky debt maturities have been refinanced or restructured. There could be near term short covering as the 731 Lex Ave debt restructuring is better understood by the market.

A couple days ago, the company filed an 8-K on the debt restructuring of 731 Lexington Ave. This transaction highlights the deal making capabilities of Steven Roth and company.

https://www.sec.gov/ix?doc=/Archives/edgar/data/0000003499/000000349925000038/alx-20251223.htm

Background - 731 Lexington is split into an office condo leased to Bloomberg on a NNN lease till 2040 and a retail condo that was mostly leased to Home Depot on a 20 year lease that recently expired. The retail condo carried $300 mm of debt which we all knew was impaired as Home Depot has confirmed that it is leaving. In addition, the Container Store which leased a large block of space on the ground floor has left years ago. One of the key risks for Alexander’s was the $500 million of debt maturing in 2025 between Rego II (a shopping center in Queens) and 731 Lex Ave retail condo. Rego II was recently refinanced into a 5 year loan after Alexander’s paid off $25 million of the maturing loan. The restructuring of 731 Lex Ave is a thing of beauty in my opinion.

Previous Write Ups - I have three previous write ups on Alexander’s which provides great background on the company. I would recommend that you read them.

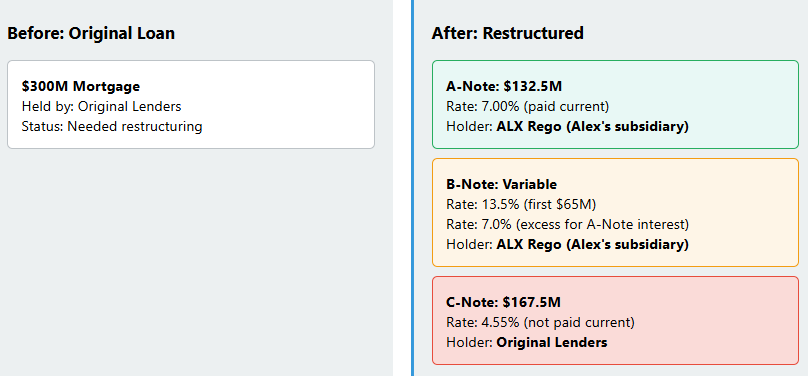

Debt Restructuring - The press release sounded confusing and it took me multiple reads to understand what was accomplished. My interpretation is that the $300 mm loan is restructured into 3 different loans. The A Note carried a balance of $132.5 mm and the lender sold the loan to Alexander’s. This is a lender exit. Basically the lender agreed to take 44% on the dollar. The B-Note will be used to fund new tenant improvements and leasing costs (TI and LC) and to pay for interest on the A-Note. The B-Note will be funded by Alexander’s and will charge an interest rate of 13.5% per annum up to $65 mm and 7% over the $65 mm balance. There is no B-Note balance currently and it will start to accrue balance and interest as the TI and LC are spent on 731 Lex Ave. The C-Note carries a balance of $167.5 mm. It is subordinate to both the A-Note and the B-Note. Distributions on future sales or refi of 731 Lex will be pari passu basis with 70% to the C-Note holder and 30% to Borrower. The C note will charge an interest of 4.55% but will be payment-in-kind (PIK) until there is a refi or sale of 731 Lex Ave. It matures in 10 years and can also be forgiven after 3 years if a refi or sale of the assets do not cover the remaining C-Note balance.

Are you confused yet? I was very confused for a couple hours. Here is a diagram. Note that Alexander’s now controls the A-Note and B-Note and the Lender is largely a junior note holder subordinated to the A and B Notes. The original lender now has minimal control on the asset.

In Plain English - My interpretation is that the lender took a 56% haircut on the loan and got 44% of the loan repaid by selling the A-Note to Alexander’s. Alexander’s will now invest capital in the property. I think capital spent on TI and LC is a good use of capital. But we’re talking about Steven Roth who is known for his deal making. He is in essence creating a 13.5% hurdle on that capital and forcing the C-Note holder (the original lender) more and more out-of-the-money over time. The longer that this C-Note stays outstanding, the more likely that it will become way out-of-the money as both the A-Note and B-Note continue to accrue interest and further subordinate the C-Note. My gut feel is that Alexander’s will let the C-Note stay outstanding for 10 years and render it potentially worthless and then pay the taxes on the write off. Notice that the interest rates on the different seniority is lopsided? Usually the more senior debt will have a higher interest rate. Yet the B-Note charges 13.5% while the C-Note accrues interest at 4.55% and also are payment-in-kind (PIK). In short, the B-Note is similar to a Debt-In-Possession loan in a bankruptcy situation that inserts itself ahead of existing debt and commands a high interest rate. While this specific asset, 731 Lex Ave, did experience bankruptcy, the bankruptcy remote nature of this loan gave Alexander’s a tremendous amount of bargaining power. It forced the lender to decide if they want to be in the business of foreclosing on the asset and then potentially spend $65 million to lease up the property OR to take a haircut and get 44% of its principal back. Alexander’s, the parent, is not liable for full payment of this loan. The only recourse the lender had was to seize the retail condo. Steven Roth is known for his astute use of non-recourse mortgages to “ring fence” liabilities to isolate the debt to each specific property.

Impact on Annual Cash Interest Expenses - Alexander’s now owns the A-Note by buying it at par from the lender using the cash on the balance sheet. We estimate that Alexander’s will save an astounding $17.3 million of cash interest expense going forward by this restructuring. At 5.1 million shares outstanding, that is an improvement of $3.39 per share in FFO. No wonder that Steven Roth responded with this quote on the Vornado earnings call when sell side analyst Alexander Goldfarb asked about dividend coverage on Alexander’s. “This is a Vornado call. I think it’s inappropriate to get into Alexander’s. We had this conversation last quarter, as I remember, there are things going on at Alexander’s that you don’t know about. And as a result of that, I quibble with your analysis. Alexander’s is going to be just fine.”

Potential Impact on NOI - We believe that Alexander’s could increase company level NOI by $10-12mm if it can successfully lease up the 731 Lex Ave retail space.

In Alexander’s 2024 10-K, it disclosed the following “During 2025, we expect to spend approximately $125,000,000 of capital expenditures at our properties.“ We have been scratching our head for a year on what this balance will be for. Building out the spaces for Burlington, DSW, and Marshalls at Rego II should not cost this much. Now that we see the B-Note balance of $65 mm for 731 Lex Ave, it makes sense. By spending just under $200 mm in buying back the A-Note and spending $65 mm in TI and LC, we believe that Alexander’s may achieve a 10% unelvered yield which would be roughly $10mm. This likely translates into $150 mm of value creation. 731 Lex Ave is not a completely empty space. It currently has Bloomberg paying $5 mm of NNN rent. In addition, there are a handful of banks, a high end chocolatier retailer, and a high end restaurant likely paying another $2 mm in rent. There is a Capital One Cafe that took over the previous H&M. This is a review on Substack.

We don’t know the property tax, insurance, and other fixed operating costs of 731 Lex Ave. But 731 Lex Ave is likely operating at break even. Empty spaces include a former Starbucks, The Container Store at the ground level has 34,000 sqft and the huge 83,000 sqft left behind by Home Depot. A great tenant would be someone like Wegman’s or WholeFoods for the Home Depot space. We’ve spoken with a retail leasing agent and the view is that the space likely has to split into smaller chunks to be fully leased. Reading the tea leaves, it is possible that Steven Roth and company already have some tenants lined up as they disclosed the $125 mm in cap ex spend in 2025. But what is the point of spending $65 mm of capital if the economics will accrue to the lenders of the $300 mm loan. I believe that Alexander’s made the lender sweat out the restructuring talk and played chicken with them while holding a huge chunk of excess cash of over $300 mm the whole time at the holdco. At a blended rental rate of $100 per sqft, the combined 117,000 sqft of space will generate about $11.7 mm of rent.

Tax Implications - I have thought about why Alexander’s and lender continue to have a C- Note rather than get paid 50 cents on the dollar and just call it a day. When debt is written off, it creates a taxable event. Let say there is no C-Note in the restructuring and the lender wrote off $150 mm of the debt, Alexander’s shareholders will have a $150 mm of taxable income in 2025 forcing Alexander’s to make a huge special dividend payment equal to 90% of that or $135 mm. By retaining the C-Note, the taxable event could be delayed by 10 years. Since Death and Taxes are the only things that are certain in life, we can use the 10 year US Treasury yield of 4.173% as the discount rate. The same $150 mm tax write off will be the equivalent of $99.7 mm 10 years from now. As a real estate investing junkie, I love to see creative tax solutions. Retaining the C Note likely allows the lender to save face and continues to hold the entire balance even though the $300 mm loan has suffered large impairment.

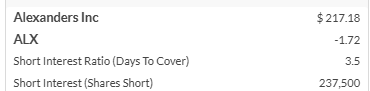

Bear Case - Alexander’s maybe the dumbest short thesis out there right now. Yet there are 237,500 shares shorted. I think the shorts may have to cover soon. Many short sellers are shorting in small sizes and do not understand the full situation. We have not heard of any detailed bear thesis.

But Vornado owns 32% of Alexander’s and Steven Roth, Russell B Jr, and David Mandelbaum collectively control about 45.9% of Alexander’s shares. There are a total of 5.1 mm shares outstanding. Hence, short sellers are short around 9% of the float which will take 3.5 days to cover. I can understand the short thesis at the beginning of the year as a two prong approach. Short sellers could have shorted based on a dividend cut and $500 million of debt maturity due in 2025. Both maturing loans have been refinanced and restructured now. The 731 Lex ave debt restructuring resulted in a $17.3 mm annual interest savings. When pushed by the sell side analyst, Steven Roth has stated that he’s not going to cut the dividend. Lastly, Rego I is on the market and the company has disclosed that it is in advanced negotiations per the recent 10-Q disclosure. If Rego I is sold, we estimate that Alexander’s may pay a $10-30 special dividend forcing the short sellers to cover their position.

Conclusion - We bought more shares of Alexander’s and it is now around a 11% position in the portfolio. We voted with our wallet. I believe that because of the holidays, people have not processed the implication of this debt restructuring. We believe that multiple catalysts have already occurred including the refinance of Rego II and restructuring of 731 Lex Ave. There is potentially a special dividend upon the sale of Rego I. We estimate that the NAV is mid $300. We will work on updating the NAV in the coming days but we want to get this update out to our subscribers. There is potentially a powder keg dynamic as the market processes the recent restructuring news. We are getting paid over 8% to wait for price discovery. We own one of the best trophy Class A office buildings on a NNN lease to one of the best possible tenants in the world in Bloomberg that won’t end till 2040. I am getting more bullish as I write out this update.